Credo $CRDO Acquires DustPhotonics for $750M — What This Deal Means for InP Players Like $SIVE

Credo just made a $750M move into silicon photonics. Every one wants a peice of AI Photonics!

At first glance, this looks like another step toward vertical integration in the optical stack, combining DSP, connectivity, and photonics into one platform.

However the deeper implication is more interesting. This deal does not remove the key bottleneck in AI infrastructure. Even if DustPhotonics planed to use of the shelf Lasers. Because while silicon photonics can route and process light, it still depends on something it cannot generate efficiently: The laser. And increasingly, that laser is based on Indium Phosphide (InP).

The Deal: Paying for Positioning, Not Revenue

Credo is acquiring DustPhotonics for approximately $750M (~ +$150m in shares). DustPhotonics generates an estimated $20–35M in annual revenue. That implies a multiple of roughly:

20x to 35x EV/Sales

This is not a valuation based on current sales. It is a valuation based on future positioning in the optical stack. Credo is not buying revenue. It is buying:

Silicon photonics capability

Optical engine design expertise

Time-to-market in 800G and 1.6T architectures

And importantly, the ability to participate in the next phase of AI infrastructure.

What Silicon Photonics Can — and Can not do

Silicon photonics is essential.

It allows:

Routing of optical signals

Modulation of data

Integration with CMOS processes

But it has a fundamental limitation. Silicon cannot efficiently generate light.

Hence:

Every silicon photonics system still requires an external laser source. At scale, and at the required wavelengths (1310nm / 1550nm), that source is almost always Indium Phosphide.

Why This Matters More After the Deal

This is the key point. The more the industry invests in silicon photonics:

The more optical engines are deployed

The more data is moved optically

The greater the demand for laser sources

In other words: More silicon photonics does not replace InP. It increases the dependency on it.

The Valuation Signal

This deal sends a clear message:

The market is willing to pay 20–35x sales

For companies positioned in the optical stack

Before full revenue scaling is visible

At the same time:

Established players like Lumentum LITE 0.00%↑ are trading at 30x multiples

Optical assets are being repriced across the board

Yet smaller InP-focused players remain:

Early

Less understood

Discounted relative to the broader trend

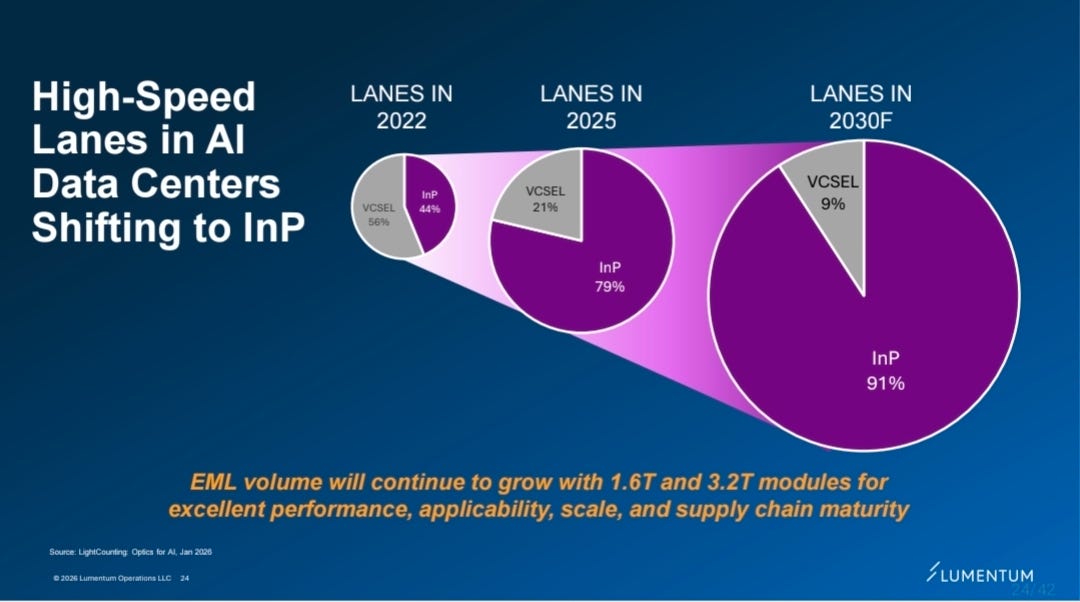

$SIVE is trading at 1/2 this approximately 15x sales. This 3-6 months old slide from Sivers CEO, clearly shows the path for $SIVE and today’s deal under pins the multiples for AI Photonics and InP Laser companies. Pre-CPO sales ramp and volumes.

In Summary

Credo’s acquisition is not just about silicon photonics. It is about securing a position in the future of data movement. And in that future:

Optical interconnects scale

Silicon photonics expands

But the bottleneck remains the same

The laser. And increasingly: Indium Phosphide (InP)

Trying to quantify the market for DFB arrays on 4” waffers. Assuming 2500 arrays per waffer (yielded). $50-150 per array.

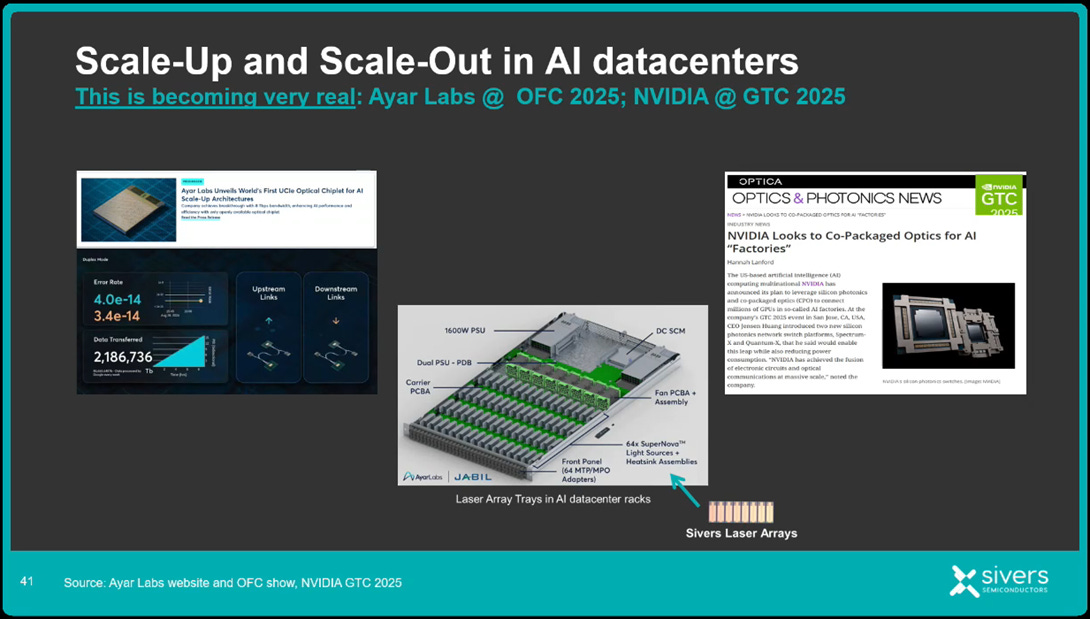

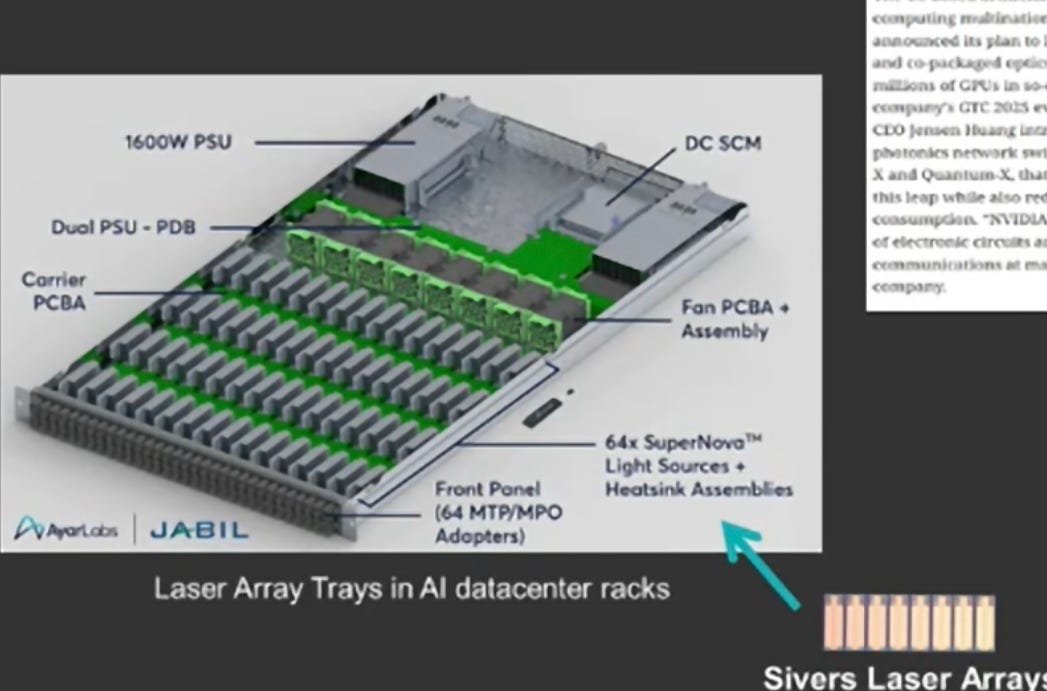

64 SuperNova per rack. With a large 100 rack AI cluster that is ~6,400+ SuperNova modules.

This gives the Following estimate:

Keep reading with a 7-day free trial

Subscribe to Anders Storm to keep reading this post and get 7 days of free access to the full post archives.