Golden Dome: Inside the Stack One of the most ambitious DoD programs ever undertaken

Could a Swedish smallcap become critical chip supplier for America's $1.2 trillion missile defense system?

Background

On May 12, 2026, the Congressional Budget Office (CBO) released a report quantifying what defense industry insiders had suspected for months. Trump's Golden Dome, the most ambitious homeland missile defense program since Reagan's SDI, will cost approximately $1.2 trillion over 20 years. That's seven times the White House's initial figure of $175 billion, and substantially higher than the Pentagon's own $185 billion architecture number.

For investors, the headline cost matters less than what it implies about scale. CBO's estimate assumes up to 7,800 space-based interceptors, an expanded sensor layer, a new battle management architecture, and a tactical communications network spanning every branch of the US military. The Missile Defense Agency has already approved 2,440 vendors under the SHIELD IDIQ contract vehicle, with a ceiling of $151 billion over ten years.

This is not one program. It is an industrial mobilization on the scale of the Apollo program or the Manhattan Project, executed through a fragmented multi-agency vendor ecosystem rather than a single prime contractor. The investment question is: who will be the actual winners?

Leonardo DRS a leading U.S. defense contractor and the primary American subsidiary of the global Italian aerospace and defense group, Leonardo S.p.A. Operating out of Arlington, Virginia describes the Golden Dome in this picture:

In February 2026, Leonardo DRS was selected as one of the prime contractors for the Missile Defense Agency's (MDA) Scalable Homeland Innovative Enterprise Layered Defense (SHIELD)

Who are obvious winners

Most defense investors are positioning around the obvious primes: Lockheed Martin, Northrop Grumman, RTX (Raytheon), L3Harris, Leonardo. They will undoubtedly capture significant value. But another interesting question is which maybe less obvious participants in the stack will see disproportionate value creation. History suggests the largest percentage returns in defense build-outs go to specialized component suppliers two or three layers below the primes, companies whose technology becomes designed-in at a level the market hasn't yet recognized.

This is an analysis of the Golden Dome stack from satellite bus down to RF chip, where the winners likely sit at each layer.

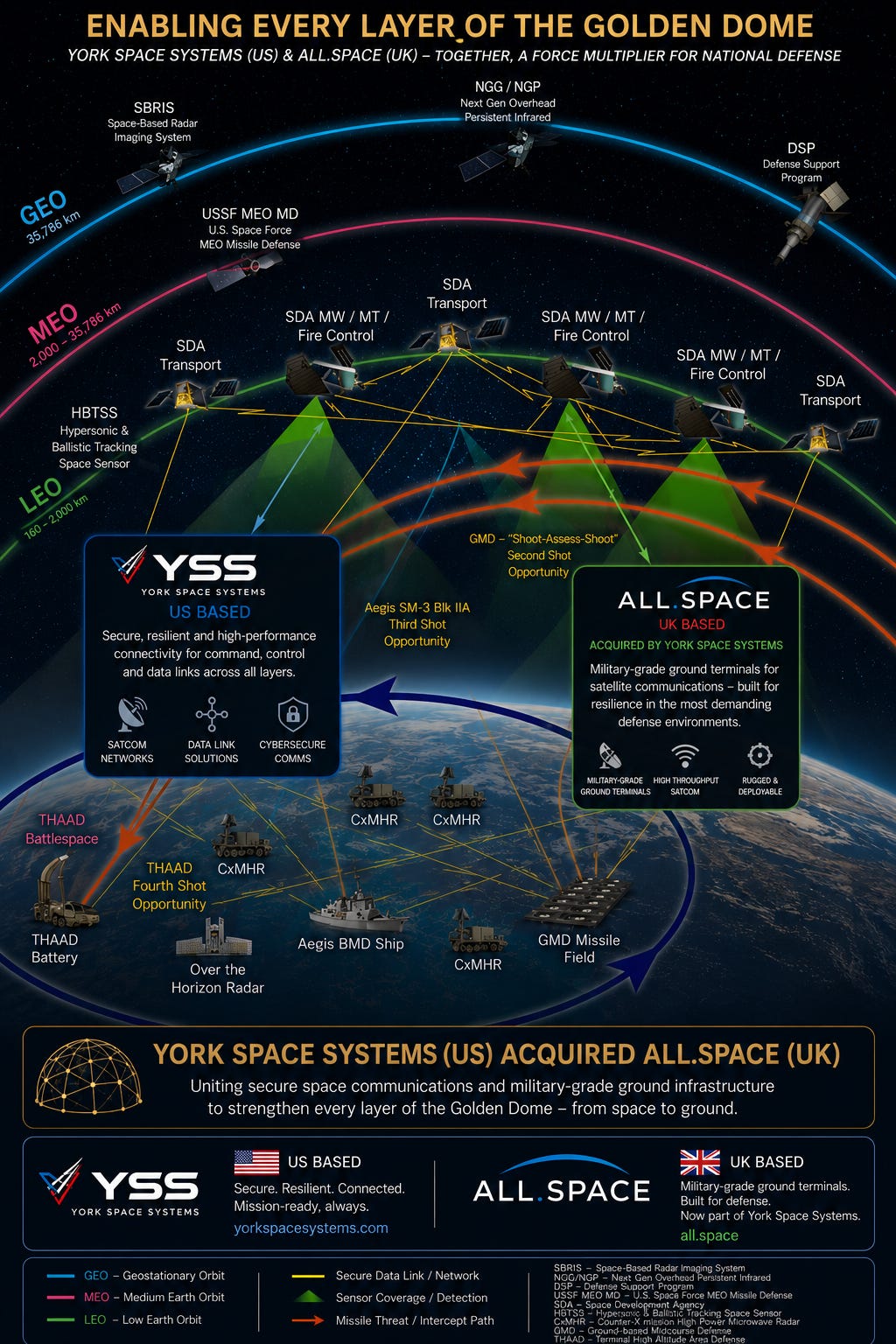

The Five-Layer Architecture

Before identifying winners, it's worth understanding what Golden Dome actually is. Public coverage focuses on the political narrative; the actual architecture is more interesting.

Layer 1 — Space-based sensors. Hundreds of LEO satellites with infrared sensors detecting missile launches within seconds and tracking exhaust plumes during the boost phase, before warheads can deploy decoys. The Space Development Agency is already building this constellation as the Transport Layer and Tracking Layer. Hypersonic and Ballistic Tracking Space Sensor (HBTSS) satellites are a key component.

Layer 2 — Space-based interceptors. The genuinely new capability. Twelve companies received OTA agreements worth up to $3.2 billion combined in late 2025 and early 2026 to develop SBI prototypes: Anduril, Booz Allen Hamilton, General Dynamics Mission Systems, GITAI USA, Lockheed Martin, Northrop Grumman, Quindar, Raytheon, SciTec, SpaceX, True Anomaly, and Turion Space Corp. First integrated flight test target: 2028. CBO estimates the SBI fleet alone could reach 7,800 units at full deployment.

Layer 3 — Ground-based strategic interceptors. Existing GBIs in Alaska and California expanded with Next-Generation Interceptor, plus THAAD, Patriot PAC-3 MSE, SM-3, SM-6, Glide-Phase Interceptor, and Aegis Ashore installations. This layer is the "known" part of US missile defense, but it's being substantially modernized.

Layer 4 — Command, control, communications, computers, and battle management (C5ISR). AI-driven decision systems operating in milliseconds. The Pentagon has described this as "data centers in space" — integrating data from infrared satellites, ground radars, and interceptor seekers into unified tracking and engagement decisions.

Layer 5 — Transport and tactical communications. The resilient, jam-resistant communications backbone linking everything together. This includes inter-satellite optical links, ground stations, and tactical SATCOM terminals deployed across Army, Navy, Air Force, and Marine Corps units.

The instinct of most investors is to focus on Layer 2 (the interceptors are the visible, glamorous part) or Layer 3 (the existing defense primes). But the most underappreciated layers — economically and strategically — are 4 and 5. Without resilient communications and AI battle management, every other layer is blind. Adversaries will not waste resources attacking interceptors directly when they can simply jam or blind the architecture that coordinates them.

Who Wins at Each Layer

Layer 1 — Sensors and Tracking

The winners here are the satellite bus manufacturers and infrared sensor specialists already executing on the Space Development Agency's Transport and Tracking Layers. L3Harris Technologies is the dominant prime, with multiple HBTSS contracts and Tracking Layer satellites in production. Northrop Grumman holds significant work on the OPIR (Overhead Persistent Infrared) program, the inheritor of legacy DSP/SBIRS missile warning capabilities. Leonardo DRS as already mentioned

Lower in the stack, infrared focal plane array suppliers — Teledyne Technologies, BAE Systems (through its US subsidiary) — provide the sensors themselves. These are not pure-play Golden Dome investments but represent solid medium-term exposure.

The dark horse: York Space Systems (NYSE: YSS). York IPO'd in January 2026 and has emerged as a credible small-satellite prime. The company has delivered 21 LEO satellites to SDA under a 2022 Transport Layer contract, won a $237 million IDIQ from US Space Force in May 2025 explicitly naming "Golden Dome demonstrations" among supported missions, and added multiple additional IDIQ awards in May 2026 explicitly tied to Golden Dome. York's vertical integration strategy (bus + ground operations + battle management + tactical terminals) is positioned for the kind of mission-package contracts SHIELD is structured to issue.

Layer 2 — Space-Based Interceptors

This is the most contested layer. SBI prototype contracts are funded. The 2028 flight test will determine which of the twelve OTA holders advance.

Possible winners: Lockheed Martin (deepest experience in missile interceptor production), Northrop Grumman (strong sensor-to-shooter integration capability), Raytheon / RTX (existing interceptor production base. Anduril is the newcomer to watch, they've moved aggressively into space systems and have political alignment with the current administration.

The lower-stack winners depend on which prime wins. Propulsion systems (Aerojet Rocketdyne, now part of L3Harris), guidance computers (specialized rad-hard processors from BAE, Cobham, Mercury Systems), and seeker electronics will all see substantial volume if the program produces at the 7,800-unit CBO estimate.

Layer 3 — Ground-Based Interceptors

Possible the most predictable layer. Lockheed Martin dominates THAAD. RTX dominates Patriot and SM-series. L3Harris holds significant ground radar work.

This is where existing defense majors capture the most committed dollars, but it's also where multiples are already extended and the surprise upside is limited. The long case for the primes is volume and longevity, possibly not multiple expansion.

Layer 4 — AI Battle Management and C5ISR

An interesting layer for technology investors, because it's the one most likely to disrupt traditional defense procurement patterns. AI-driven battle management at the speed required, millisecond decisions across thousands of potential threats, is not something traditional primes have demonstrated.

The natural winners are Palantir Technologies (Mission Maven and AIP platform are already deployed in DoD contexts), Anduril Industries (Lattice software platform), and emerging firms like Shield AI and Scale AI. Larger players include Booz Allen Hamilton for systems integration work.

The hardware enablers for AI in space, radiation-hardened GPUs, secure compute modules, represent a smaller but interesting sub-segment. Mercury Systems, Kratos Defense, and Curtiss-Wright all have positions here.

Layer 5 — Tactical Communications

Here is where the analysis gets genuinely differentiated. Tactical SATCOM terminals are the "boring" component some investors skip, except they're the component without which the entire architecture is inert.

Viasat, Hughes (EchoStar), L3Harris, and General Dynamics Mission Systems are the incumbent prime suppliers. They will all win significant volume. Iridium Communications has unique low-latency Ku-band coverage that complements the architecture.

But the technology shift in tactical terminals favors a smaller, newer player. The traditional terminals use mechanically-steered antennas. Modern tactical SATCOM demands electronically steered arrays (ESAs), flat-panel antennas with no moving parts, capable of tracking multiple satellites simultaneously and providing "make-before-break" connectivity as satellites pass overhead.

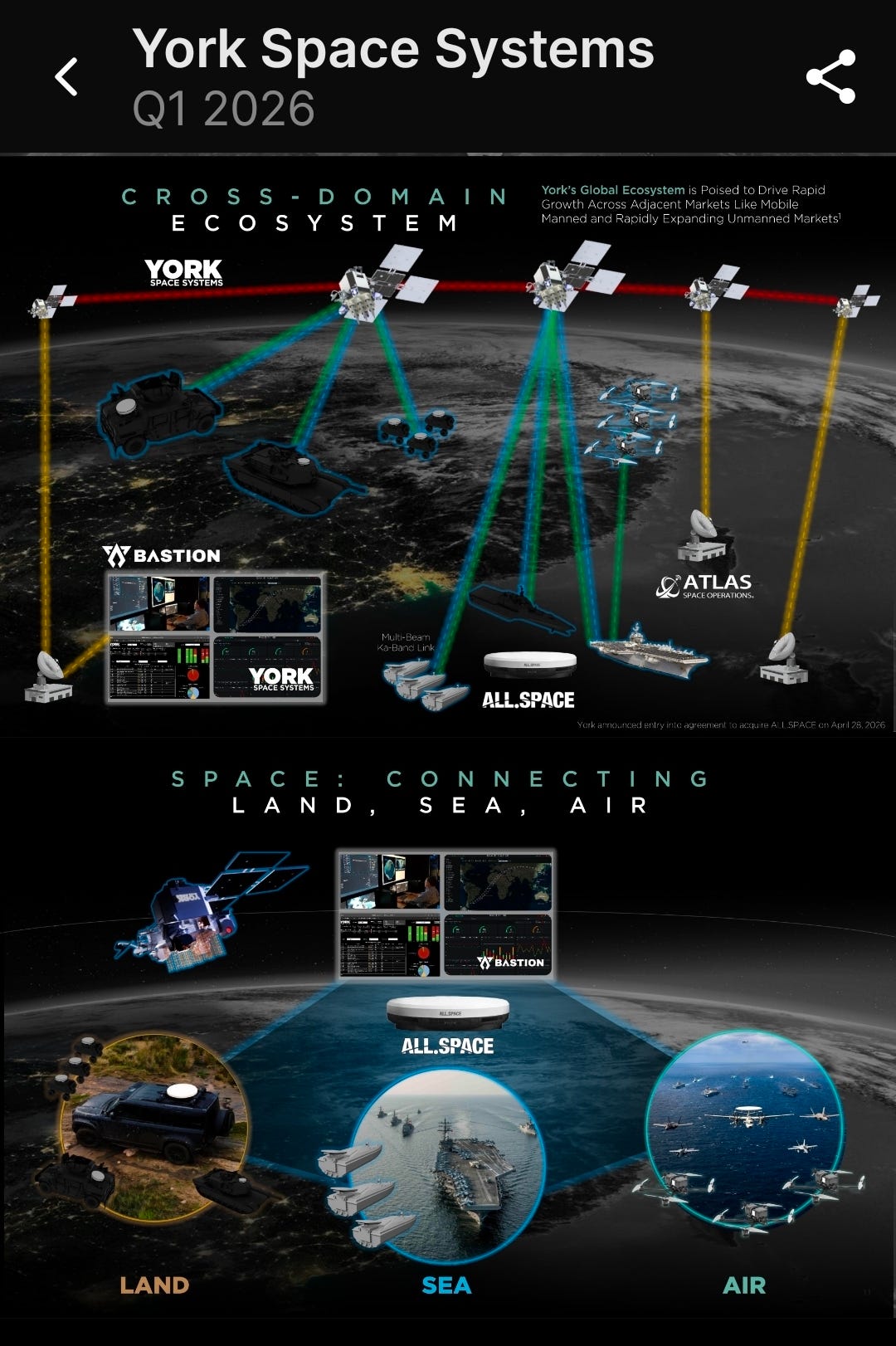

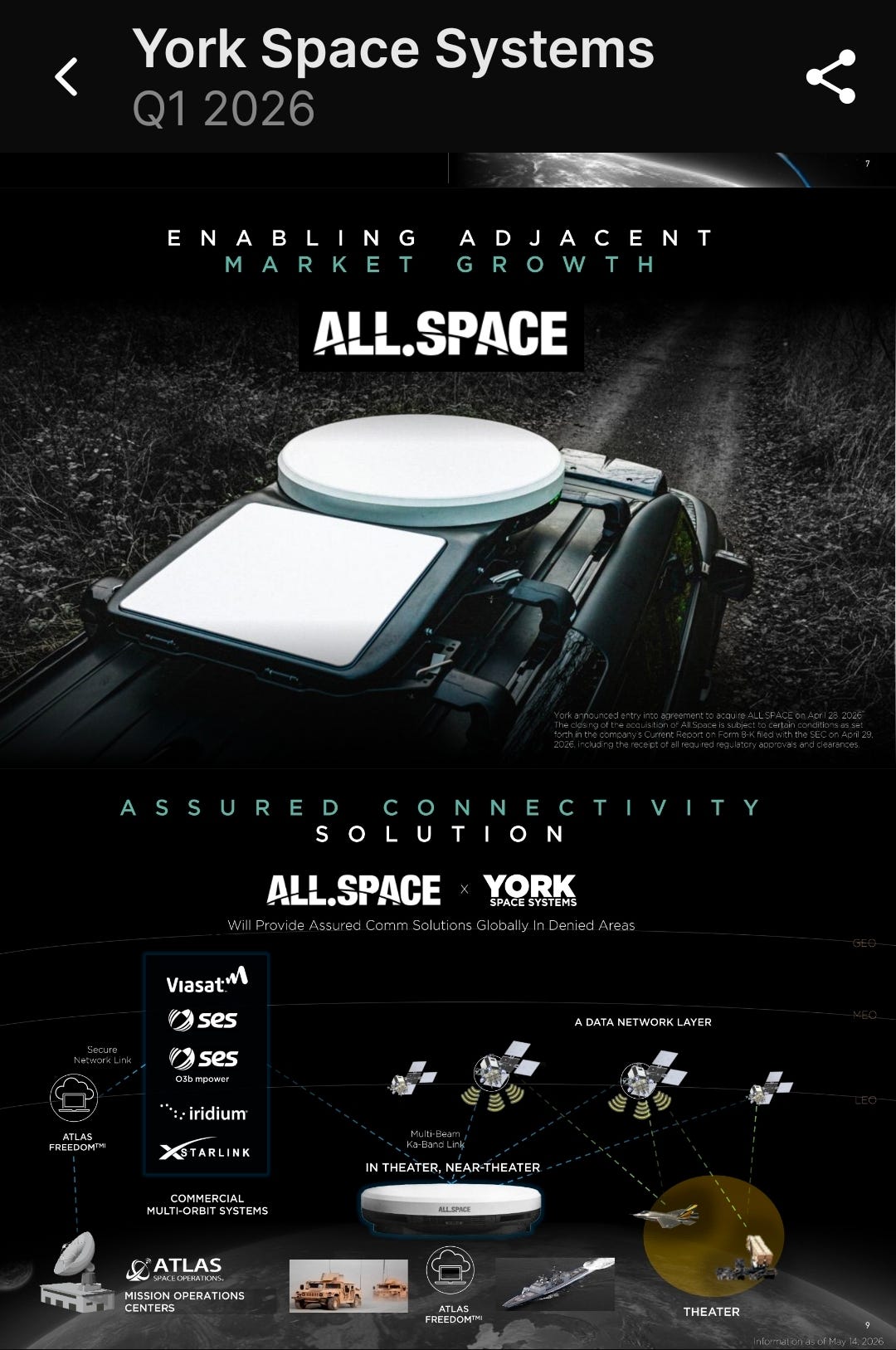

York Space acquired All.Space

ALL.SPACE is the leader in multi-orbit, multi-link SATCOM solutions. They have successfully completed testing under the U.S. Army’s Next Generation Tactical Terminal (NGTT) program. The company’s Hydra MAX terminal has been validated as a first-of-its-kind solution capable of delivering seamless, simultaneous, and resilient connectivity across Low Earth Orbit (LEO), Medium Earth Orbit (MEO), and Geostationary Orbit (GEO) satellite networks – all while on the move.

“With this acquisition, York is creating a complete communications ecosystem that operates in contested environments across commercial and government networks,” said Dirk Wallinger, CEO of York. “The addition of ALL.SPACE brings a world-class team whose proven leadership and technical excellence will be key as we scale these capabilities for our customers.”

All.space ESA terminal is purpose-built to align with the Department of Defense’s Joint All-Domain Command and Control (JADC2) objectives, Hydra MAX supports a Modular Open Systems Approach (MOSA), enabling rapid integration with future constellations, including Telesat Lightspeed once Hydra MAX is certified for the network. With multi-beam transport diversity, integrated SD-WAN resilience

What major technology is behind a ESA terminal

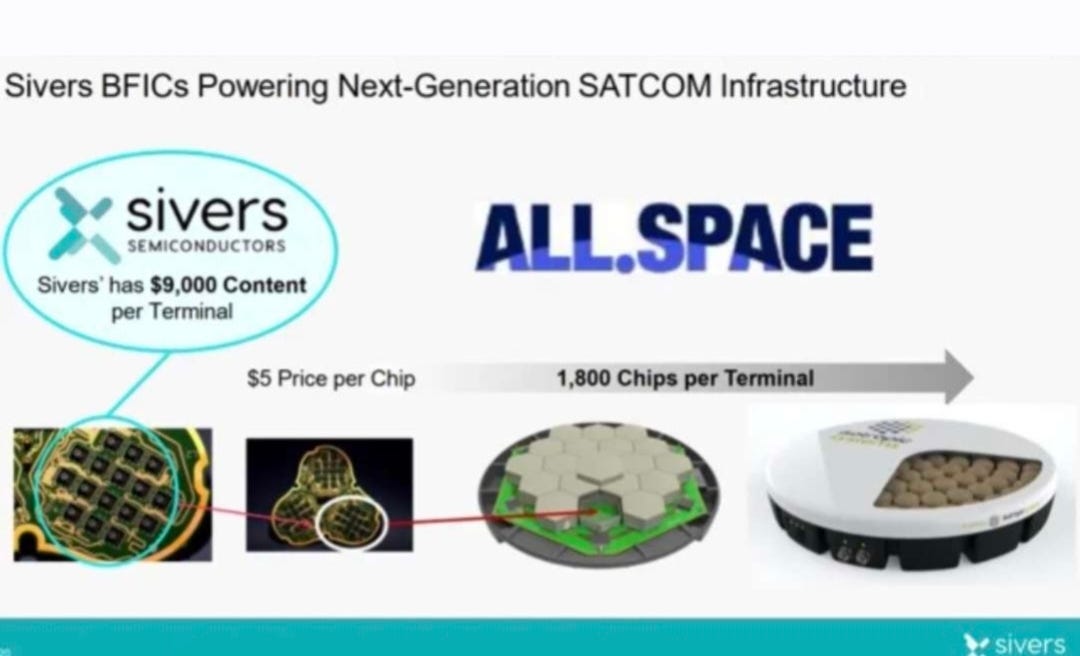

ESA terminals require massive numbers of beamforming RFICs, specialized chips that electronically steer the radio beam. This is a small, technically demanding market dominated by perhaps five suppliers globally. And one of them, almost no defense investor has heard of.

The Component Layer in terminals

Look at any modern high-end phased-array antenna and you'll find roughly 1,000 to 2,000 beamforming chips arranged in a grid pattern, each contributing a small piece of the steering signal. The chip count scales with antenna size and capability. A high-end military ESA terminal capable of simultaneous multi-orbit connectivity contains around 1,500 - 2,000 beamforming ICs.

The market for Ka-band beamforming RFICs is dominated by three companies: Qorvo (acquired Anokiwave in 2022), Renesas Electronics (through its IDT acquisition), and Sivers Semiconductors (NASDAQ Stockholm: SIVE). Each has different strengths. Anokiwave/Qorvo has been the volume incumbent and started SATCOM BFIC development long before SIVE. Sivers has captured a position in the most high-performance defense segment that few DoD investors has noticed. Via the acquisition of Mixcomm.

Sivers Semiconductors is a Sweden based fabless chip designer. Its Wireless division produces Ka/Ku-band beamforming RFICs and integrated ESA panels. Its Photonics division produces InP DFB lasers for AI data center optical interconnects, a separate business, see my other substack on this link .

Important fact: Sivers is the single-source supplier for the beamforming chips in the All.Space Hydra tactical SATCOM terminal.

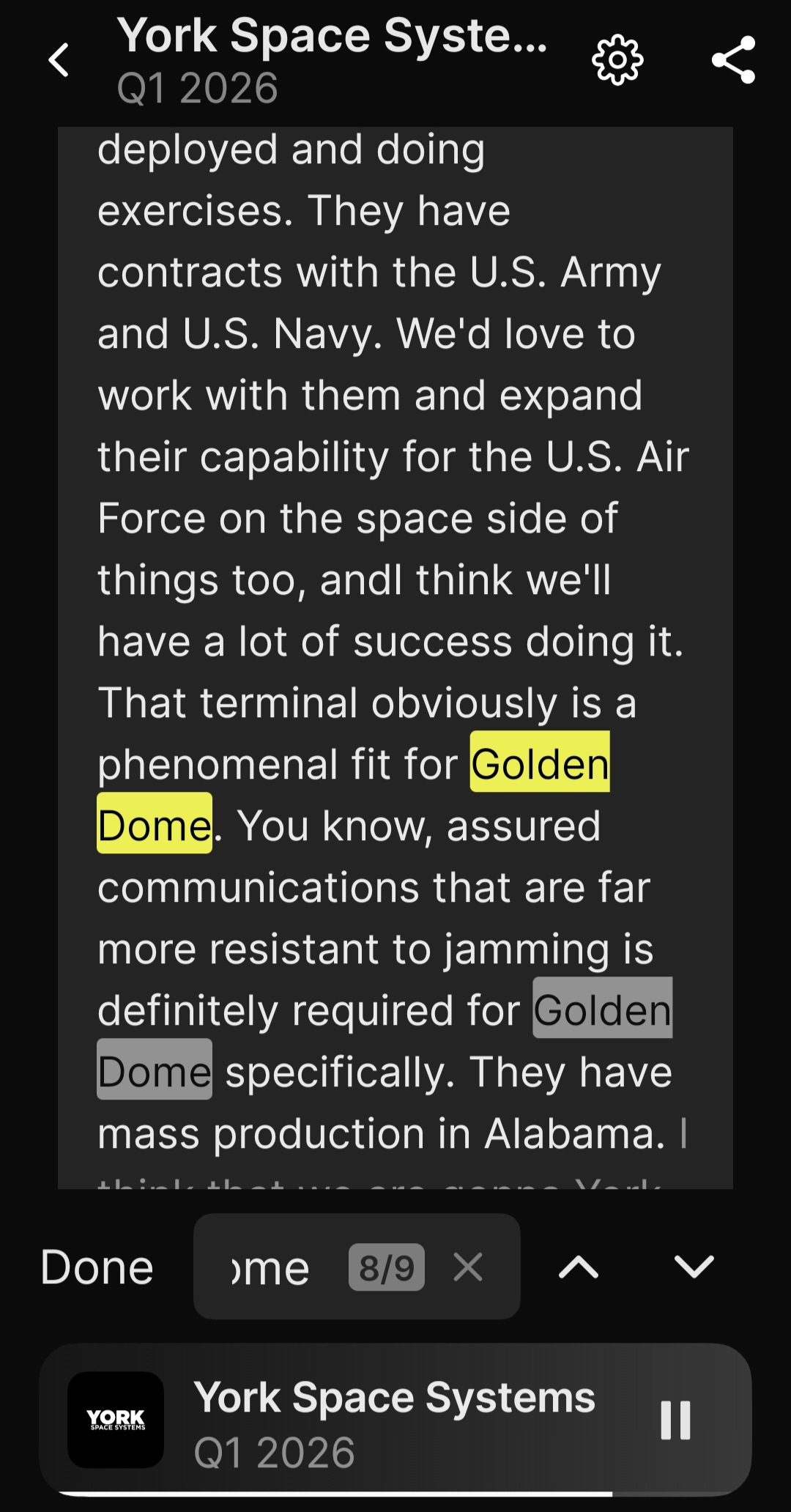

All.Space, formerly Isotropic Systems, builds what is generally considered the most advanced military SATCOM terminal in the world. The Hydra connects to four satellites simultaneously across different orbits and bands. It is jam-resistant by design. It already has contracts with US Army, US Navy, and NATO, and has a mass production facility in Alabama. On April 28, 2026, York Space Systems announced the acquisition of All.Space for $355 million.

On York's Q1 2026 earnings call, CEO Dirk Wallinger described Hydra as "a phenomenal fit for Golden Dome. You know, assured communications that are far more resistant to jamming is definitely required for Golden Dome specifically."

This connects three things that few investor have connected:

York is a Golden Dome contractor with $237M+ in IDIQs explicitly naming the program

All.Space is now York's tactical communications subsidiary

Sivers is single-source supplier inside All.Space's flagship terminal

The unit economics

Sivers' own investor presentations confirm the chip economics:

Approximately $5 per chip for Ka-band. 1,800 chips per Hydra terminal, $9,000 of Sivers content per terminal

The new dual-band Ka/Ku chip will have a higer ASP raising per-terminal content. The dual-band capability is significant it expands Hydra's addressable market to include legacy Ku-band constellations including portions of the Viasat fleet, older WGS, and most maritime SATCOM systems.

Single-source positioning in DoD-qualified terminals is not a casual vendor relationship. Re-qualifying an alternative beamforming RFIC requires complete RF front-end redesign, re-certification against MIL-STD-810, MIL-STD-461, and MIL-STD-704, plus re-testing across Army, Navy, and NATO programs that already have Hydra in service. Industry-standard timeline: 18 to 36 months. Industry-standard cost: $5 to $20 million per re-qualification. Defense terminal production lifecycles run 15 to 20 years.

All.Space is, in practical terms, economically locked into Sivers for the foreseeable production lifecycle of Hydra.

Why "Swedish supplier" is the wrong framing

The natural objection is: "How does a Swedish company become single-source in a DoD-critical terminal?" The answer reveals one of the most underappreciated facts about Sivers' actual structure.

Sivers Wireless is fabless. The chips are designed by engineers in Sweden and in New York (acquired through MixComm in 2022), but they are manufactured by GlobalFoundries at facilities in Vermont and upstate New York. GlobalFoundries (NASDAQ: GFS) is one of the few DoD-designated "trusted foundries" certified for sensitive defense electronics, and was a minority investor in MixComm before the Sivers acquisition.

From a DoD supply chain perspective, Sivers' chips are produced in the United States by a trusted American foundry, packaged and tested in American facilities, with design IP partially held by US-based engineers in New York. The "Swedish" label refers to the parent company's listing venue and headquarters — not the production trust chain.

This is precisely the supply chain structure the CHIPS and Science Act was designed to support. And the Pentagon has noticed.

The Second Path — CHIPS Act

Sivers may also have a second, independent path into Golden Dome that has received even less investor attention.

In October 2024 and January 2025, Sivers signed contracts with the Northeast Microelectronics Coalition Hub under the US CHIPS and Science Act's Microelectronics Commons program. The contracts, executed through the Naval Surface Warfare Center Crane Division, fund two parallel chip development

programs:

Electronic Warfare full-duplex arrays, chips capable of transmitting and receiving simultaneously on the same frequency through ultra-precise self-interference cancellation

5G/6G FR3 beamformer ICs — mid-band beamforming for both commercial and defense applications

First-year funding: $11.6 million. Total program value if renewed across three years: approximately $30 million. Link to deep dive here.

The partner list, named explicitly in Sivers' own press releases, is the interesting part: BAE Systems, Raytheon, MIT Lincoln Laboratory, Columbia University, and Ericsson.

The second round of the awards was released 19th of May: $6.6M Year 2 Program Award through NEMC Rewards Strong Execution and Reinforces Growing Momentum in Modernizing U.S. Defense Infrastructure Using Sivers Technology.

The CHIPS Act designation matters beyond the funding itself. Sivers has been assessed as strategically important enough that the US government channeled federal money through a Northeast hub to a Swedish-parented company.

Sivers now has two independent paths into Golden Dome. Path A: single-source supplier to All.Space, acquired by York, building tactical terminals for the program's communications layer. Path B: CHIPS Act-validated component supplier.

Conclusion

The Golden Dome stack has obvious winners and hidden ones. . The hidden winners are smaller, more specialized, and harder to identify because they sit two or three layers below the primes in technology stacks that defense generalists don't analyze.

Among these hidden winners sit the component suppliers behind tactical SATCOM terminals, specifically the beamforming RFICs that make modern ESA terminals possible. York's acquisition of All.Space was not random. The acquisition gives York vertical integration into the communications layer of the very architecture the program needs. And All.Space, in turn, is single-source dependent on Sivers Semiconductors for the chips that make Hydra work.

Golden Dome applications also effect the next layer like chip manufacturing through GlobalFoundries.

The thesis is not "AI infras”

The thesis is not "AI infrastructure will continue" or "Golden Dome will be funded." Both are true and neither is unique insight. The thesis is that the connections between three concurrent macro trends, hyperscaler AI capex, missile defense modernization, and US semiconductor reshoring, flow through a single Swedish-listed microcap whose dual-listing on Nasdaq is on the way.

On May 22, 2026 — one day before this is published — Sweden and the United States signed a new memorandum of understanding on technology cooperation covering AI, defense innovation, space, and quantum technology. It is a strong signal that the two countries are formalizing strategic alignment in precisely the domains where Sivers operates.

This is what asymmetric opportunity looks like before consensus arrives.

Anders Storm

23 of May 2026

Disclosure: This analysis is for informational purposes only and does not constitute investment advice.

The author has positions in Sivers, YSS and GlobalFoundries. Readers are highly recommended to conduct their own due diligence on any investment.

This is fantastic. Thanks Anders.

Great insight. Thank you for all that you do.