Sivers Semiconductors $SIVE - SATCOM Timeline: From RFQ Loss to Ramp 2020-2027

The path and creation of the second leg in $SIVE - SATCOM

Table of Contents

The Trigger: Losing the RFQ

Strategic Response: MixComm Acquisition

NRE Phase Begins

First System Validation: All.Space

European Traction: Thorium Space

Institutional Backing: ESA Programs

Expanding NRE Pipeline

U.S. Positioning: DoD & Ecosystem

The Current Phase: Pre-Ramp

Key Takeaway

1. The Trigger (2020–2021): Losing the RFQ

Before acquiring MixComm, Sivers was invited to an SATCOM beamformer RFQ.

They lost. To MixComm.

That moment exposed a clear gap in beamforming IC capability — and became the trigger for the next move.

2. The Strategic Response (2021): Acquiring MixComm

Sivers responded by acquiring MixComm.

This added:

Advanced BFIC technology

mmWave expertise

U.S. presence DoD access

3. The NRE Phase Begins

Following the acquisition, Sivers began securing NRE (Non-Recurring Engineering) engagements. Read my other post about the significance of NRE to fund a business in EU due to lack of capital. The long game is always the balance of getting NRE funds and keep the IP to make standardize products. This is not a consulting business, this is funding to become a product-based business.

These signal:

Design-ins

Early validation

Future production potential

PR example: Biggest NRE project

4. First System Validation: All.Space

One of the most important milestones:

Sivers BFICs used in All.Space ground terminals

Advanced multi-beam SATCOM terminal

High BFIC content per unit

Real-world validation

5. European Traction: Thorium Space & Others

Sivers expanded into the European SATCOM ecosystem:

Thorium Space

Other EU partners

This builds:

Regional exposure

Defense relevance

6. Institutional Backing: ESA Programs

Sivers participates in ESA-backed (European Space Agency) programs:

Technology validation

Funding support

Strategic alignment

7. Expanding NRE Pipeline

Sivers continues to announce:

Multiple active NRE engagements

Expanding customer base with well-known names

Transition path: NRE → Design-in → Qualification → Production

8. U.S. Positioning: DoD & Ecosystem

Through MixComm and U.S. presence:

Access to DoD ecosystem

Alignment with CHIPS Act

Partnerships with major players

Entering Asien market via Doosan

Looking across the timeline:

Technology gap → solved

Validation → achieved

Ecosystem → established

Pipeline → expanding

End customer Qualification and approval by US Army

What remains: Production ramp and volume production!.

10. Key Takeaway

This is not a new story. It is a multi-year build-up now approaching commercialization.

NRE → Design-in → Qualification → Ramp →Production

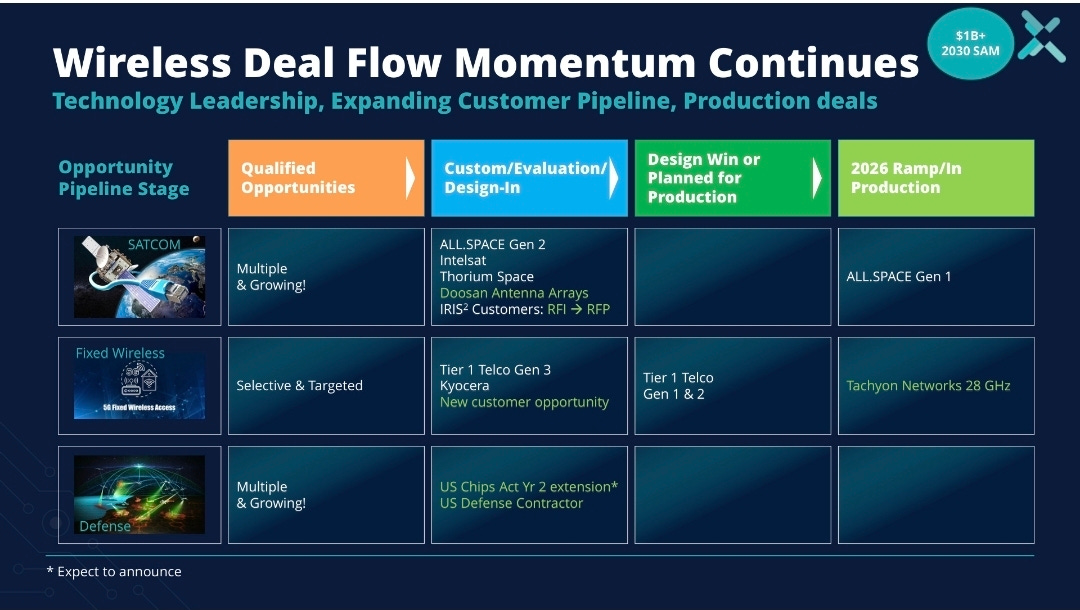

Sivers has already moved through the first 3 stages. Sivers management estimate $1B SAM in Q4 webinar Februari 2026. Full deal flow below:

Final Thought

The market focuses on when revenue shows up.

But in SATCOM: The timeline tells you when the ramp is coming and Product sales has increased over the last years to support customer qualification.

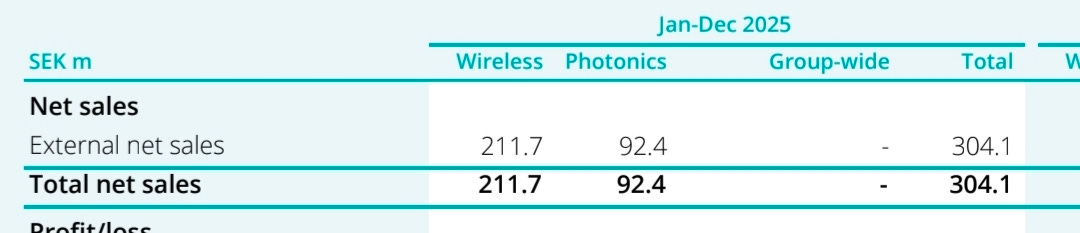

Wireless BU is 2x Photonics today with $23m in Net sales 2025 16% Product and 84% NRE. Where NRE shall be seen as investments in Future products sales funded by the customer. This is “To have your cake and eat it too”!

2025 sales by BU:

Sivers seems to approach the ramp phase within SATCOM and AI Photonics at the sametime.

Anders Storm

Former CEO of Sivers for 8 years.

Disclaimer: This newsletter is NOT investment advice. This is my analysis based on publicly available information; not investment advice. I have no current relationship with the company. The aim of this newsletter is to provide subscribers with basic and simplified insights about the semiconductor industry and its participants. Articles will be published semi-frequently.